Att. Minister

In its decision on 23 June 2004, the Government authorised Minister Gunnar Lund to assemble a committee to evaluate the function of the premium pension system (directive 2004:77). Backed by the same authorisation, Professor

To assist the committee in the capacity of experts, the following individuals were appointed as of 2 September 2004: acting Chief Economist Daniel Barr, Senior Advisor Lars Gavelin, Managing Director Reinhold Geijer, Department Director Catrina Ingelstam, Professor

Jenni

Anna Florell has acted as committee assistant.

The committee, which assumed the name Premium Pension Committee (Fi 2004:13), hereby submits its report Svårnavigerat? Premiepensionssparande på rätt kurs (SOU 2005:87). (Difficult waters? Premium pension savings on course). This completes the assignment.

29

SOU 2005:87

Specific statements made by some of the experts have been enclosed in the report.

Stockholm, Sweden October 2005

/Dimitrios Ioannidis

Joakim Jansson

Thomas Norling

30

Extended summary

The Riksdag decided in 1998 to adopt the new pension system consisting of guarantee pension, income pension and premium pension. Pension rights are earned annually as 18.5 per cent of the sum of earned

The Premium Pension Authority (PPM) was founded to administer the premium pension system. PPM is to keep an individual premium pension account for each pension saver that shows the development of the saver’s holdings in the system. The Sjunde AP- Fonden (Seventh Swedish National Pension Fund) was also set up to manage the Premiesparfonden (the Premium Savings Fund), where money was invested for those pension savers who opted not to choose. Sjunde

The premium pension system is funded, which means it is possible for pension savers to receive a higher pension given that the return in pension investments exceeds the growth of labour income in the society. It is also possible to spread the risks internationally since pension savers can invest in the financial market. The distinguishing feature of the premium pension system is that pension savers themselves carry investment risks and make investment decisions. Savers can thereby adjust the risk levels for their premium pension savings to their specific life situation.

In its operations, PPM acts as a unit linked insurance company, where asset management is conducted in investment funds that have applied to PPM for registration and are handled by independent fund managers. The unit linked insurance model means that PPM is owner in investment funds where the money is invested. Pension savers can opt to invest their money in as many as five

31

| Extended summary | SOU 2005:87 |

funds on the PPM fund market. The basic requirements for registration stipulate for instance that the fund manager must have a permit to conduct fund business in accordance with the Investment Funds Act and is subsequently monitored by the Swedish Financial Supervisory Authority (Finansinspektionen) or comparable authorised foreign agency. A fund can be registered if the fund fulfils requirements corresponding to those in the UCITS Directive.

If the pension saver does not select a fund, the money is invested in Sjunde

Premium pension can be drawn starting the month the pension saver turns 61. There is no set time when pension must be collected at the latest. Premium pension is lifelong and calculated equally for women and men. Pension is calculated based on the balance in the premium pension account. When drawing pension, the pension saver has the alternative to keep his/her account balance invested in securities funds. The saver can also receive his/her premium pension in the form of a life annuity as a guaranteed amount.

According to the official document for appropriations, PPM’s operations are to gradually be covered by fees extracted from the pension savers’ premium pension accounts. Every year PPM invests considerable amounts (over SEK 23 billion in 2005) in funds for 5.4 million pension savers. PPM handles a large part of the administration and information that otherwise would befall fund managers. PPM negotiates with fund managers registered in the system for discounts on fees for manager services. PPM receives rebate on the management fees extracted by fund managers which are based on the size of the funds’ fees and PPM’s total holdings in the funds. The rebates that fund managers repay to PPM are reinvested in full in each respective fund on behalf of the pension savers.

32

| SOU 2005:87 | Extended summary |

The committee’s assignment

The committee’s assignment entails identifying any problems associated with actual and expected difficulties in supporting individual saver’s decisions to choose and switch funds through information and guidance.

The committee is also to assess to what extent more detailed information and guidance can improve the results and reduce the risks for systematic poor outcomes and propose related measures.

The committee is also to review the design of the system in respect to the scope of the fund selection and how it is compiled and propose measures that facilitate the selection process for individual savers and reduce the risk for systemic poor outcome.

Furthermore, the committee is to assess the system’s costs in the form of fees for participating fund managers and assess the consequences of the proposals submitted for the system’s collective administration costs.

Finally, the committee is to consider and propose improvements for the individual in conjunction with transferring to life annuity.

The basis for the committee’s work

The first round of choice in the Premium Pension System was in 2000 and it was preceded by a period of very strong growth on the stock exchange, which was followed by a period of dramatic declines in share prices after the first round. The committee’s assignment should be viewed against this background. At the same time, it should be noted that the premium pension system does function well and is reasonably cost effective. The basis for the committee’s work has therefore not been to create a new system but to propose improvements in the current premium pension system.

Based on the guidelines given to the committee, the committee has concluded that the premium pension system will continue to be a unit linked insurance system where asset management is carried out in investment funds administrated by independent private or public fund managers. Public managers must comply with the same terms and conditions and in full competition with the private managers. The Premium Pension System will also continue to be designed as an open system. This means that a fund manager that fulfils the requirements is in principle free to register its funds in the

33

| Extended summary | SOU 2005:87 |

system and that PPM when registering the fund will not make any assessment as to whether it is appropriate that the fund is in the system. PPM will instead take

The committee understands that PPM’s ongoing activities are governed by the pension savers’ needs. One guideline should be that pension savers have a better chance to manage their investments so they receive a high premium pension. The committee has as its basis chosen to propose as few changes in the regulations as possible and allow PPM to utilise the discretion already at the authority’s disposal.

Pension savers’ management results

Since new pension rights are earned and new money deposited each year, the fall in the stock exchange that occurred at the start of the period becomes less significant. In 2005, the fund capital value for the first time exceeded the combined deposits and the increase in value totalled SEK 21 billion at the close of September.

Accumulated deposited amount and fund capital, SEK billion

| 200 | 181 | ||||

| 160 | 160 | ||||

| 120 | |||||

| 80 | |||||

| 40 | |||||

| 0 | |||||

| 2000 | 2001 | 2002 | 2003 | 2004 |

Source: PPM

34

| SOU 2005:87 | Extended summary |

At the close of September 2005, 89 per cent of the pension savers were on the credit side of their premium pension accounts. Pension savers’

Pension savers’ average outcome,

| 30% | |||||||||||||||

| 20% | Internränta | ||||||||||||||

| 10% | |||||||||||||||

| 0% | |||||||||||||||

| Tidsviktad | |||||||||||||||

| avkastning | |||||||||||||||

Source: PPM

Pension savers’ management

A comparison with other pension systems reveals that the Swedish premium pension system has a large portion of active savers. In the first round of choice in 2000,

35

| Extended summary | SOU 2005:87 |

miesparfonden. The level of activity in the system has however dropped over time.

Share of

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 |

| 33 % | 72.4 % | 85.9 % | 91.7 % | 90.6 % | 92 % |

Source: PPM

Both pension savers with money in the Premiesparfonden and those in the fund market have to a large extent refrained from changing their choices. There is however a tendency for greater activity. During 2004, almost 6 per cent of the pension savers had switched funds. At the close of April 2005, a total of 12 per cent of the pension savers had switched funds at least once. The number of fund changes is increasing which to a certain extent is influenced by the occurrence of advisory firms that continuously switch funds for pension savers.

Pension savers have primarily invested in shares. Up until 2003, those that made active choices invested almost

The allocation between shares and interest at an aggregated level does not however reflect the entire distribution at individual levels. Over half of the

36

| SOU 2005:87 | Extended summary |

Distribution of portion in shares at individual level,

| Proportion | |||||||||||

| 45% | |||||||||||

| 40% | |||||||||||

| 35% | |||||||||||

| 30% | |||||||||||

| 25% | |||||||||||

| 20% | |||||||||||

| 15% | |||||||||||

| 10% | |||||||||||

| 5% | |||||||||||

| 0% | |||||||||||

| 0% | % |

% |

% |

% |

% |

% |

% |

% |

% |

% |

100% |

Portion in shares

Source: PPM

An analysis of which

However, analyses also reveal signs that simple

It can be difficult for pension savers to evaluate various fund managers. Subsequently, pension savers have a tendency to choose well know fund companies, which can for instance mean that domestic fund companies are chosen ahead of foreign fund companies and fund companies that have an established brand name are selected ahead of fund companies with a weaker brand name. PPM

37

| Extended summary | SOU 2005:87 |

has compared the popularity of Swedish and foreign fund companies and notes that only about 8 per cent of the total capital is invested in funds managed by foreign fund companies. At the same time, the analysis shows funds managed by Swedish fund companies on an average to a greater extent show lower growth compared with the relevant index than foreign fund companies’ funds.

Lack of knowledge and participation

According to a survey presented by Demoskop in April 2005, only 6 per cent fully agree with the statement that they have sufficient knowledge to manage their premium pension savings. A further 11 per cent rate themselves a 4 on a scale of

Pension savers’ perceived knowledge “I have sufficient knowledge to handle my premium pension savings.”

Source: Demoskop 2005.

5=Agree completely 3=Don’t know 1= Disagree completely

38

| SOU 2005:87 | Extended summary |

In a comparison with other systems, the Swedish premium pension system has a high portion of active savers. Increasingly fewer first-

Evaluation of the premium pension system’s costs

The average investment management fee for the funds in the premium pension system (including Premiesparfonden) is currently 0.39 per cent of the managed assets after rebate. Costs for PPM’s administration (PPM fee) in 2005 correspond to a fee of 0.22 per cent. At present, the collective withdrawal for fees for the average saver is just over 0.6 per cent of the managed assets. Administration fees as a portion of the managed assets will drop over time as the assets in the system grow and the cost levels for PPM’s activities stabilise. In the same way, average investment management fees can be expected to drop in time. The combined annual withdrawal for fees in relation to managed assets is expected to fall to about 0.3 per cent in 2020, of which 0.25 can be attributed to investment management fees and 0.05 to PPM’s administration costs.

39

| Extended summary | SOU 2005:87 |

Forecast of fees in the premium pension system

| 0,70% | |||||||||||||||

| 0,60% | |||||||||||||||

| 0,50% | |||||||||||||||

| 0,40% | |||||||||||||||

| Fee | Total fee | ||||||||||||||

| 0,30% | |||||||||||||||

| Average management fee after rebate | |||||||||||||||

| 0,20% | |||||||||||||||

| 0,10% | PPM fee | ||||||||||||||

| 0,00% | |||||||||||||||

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| year | |||||||||||||||

Source: PPM

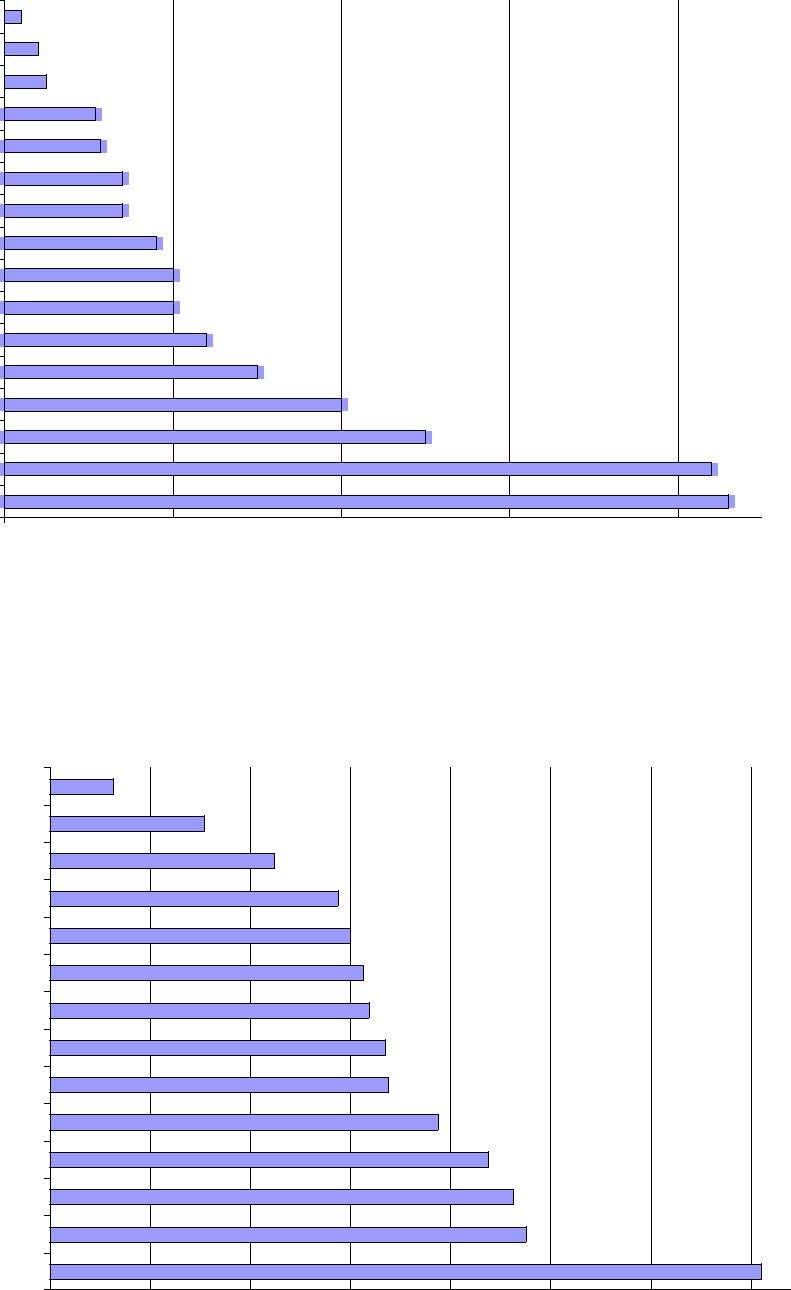

An international comparison shows that withdrawal for fees from savers in the premium pension system is low overall. The assessment is based on a comparison of, in part the system’s withdrawal of fees from future pension and, in part the system’s fees in relation to managed assets. However, there are systems that rank even better.

40

| SOU 2005:87 | Extended summary |

Relation between total fees and assets in various systems

USA: TSP

Denmark: atpValg

Premium pension 2020

Denmark: medValg

Denmark: selvValg

Premium pension 2005

Australia: "corporate"

UK: "personal"

Australia:

UK - "stakeholder"

Chile

UK - "personal"

Australia: "master trust"

Mexico

Argentina

Poland

| 0% | 1% | 2% | 3% | 4% |

Source: Whitehouse (2001), James (2005) and ATP

Portion of fees withdrawn from future pension

Denmark: atpValg

Premium pension

Australia

Chile

Denmark: medValg

Denmark: selvValg

Poland

UK - "stakeholder"

Mexico

Argentina

UK - "personal"

| 0% | 5% | 10% | 15% | 20% | 25% | 30% | 35% |

Source: Whitehouse (2001), James (2005) and the committee’s own calculations

41

| Extended summary | SOU 2005:87 |

There are several different ways of organising a funded pension system. One alternative is that the state acts on the institutional market and procures the management for all pension savers at wholesale prices with quantity discounts. Pension savers then select a risk level (asset allocation) but not a manager. The other extreme is that pension savers each individually select investment funds at consumer prices and without quantity discounts.

The premium pension system is somewhere in the middle. PPM serves as a clearinghouse where pension savers and participating fund managers meet. Pension savers choose the managed investment funds but PPM is the owner of the fund units. Since PPM is the only owner of the funds in the system, PPM is in a position to demand a quantity discount from the participating fund managers.

The international comparison between the premium pension system and other systems with individual accounts shows the premium pension system has low costs, even when compared with systems that provide more limited freedom of choice in respect to investment alternatives. At the same time, the comparison shows there are systems with more limited freedom of choice and therefore lower costs compared with the premium pension system. With the price reduction model adopted by PPM, the fee after rebate that PPM pays on the fund market resembles the possible wholesale price. The premium pension system’s discount model therefore fills a central function as a

Design of the premium pension system

The premium pension system is said to consist of two parts: the information pension savers require for their investment choice and the system’s investment alternatives, i.e. the funds participating in the system. Pension savers face as

42

| SOU 2005:87 | Extended summary |

Present premium pension system

PPM fund market

Capital

market

Premiesparfonden

| Informatíon | Product |

Based on their knowledge and participation, pension savers can be divided into three different groups that each constitutes the primary target group for one of the following management solutions:

1.Pension savers that feel they have neither the knowledge nor the commitment to design and manage their own fund portfolio are the primary target group for Premiesparfonden (the system’s default alternative).

2.Pension saves that feel they have the commitment to design and manage their own fund portfolio but insufficient knowledge to do so are the primary target group for choosing and switching funds on the PPM fund market but with guidance.

3.Pension savers that feel they have sufficient knowledge and commitment to design and manage their own fund portfolio are the primary target group for choosing and switching funds on the PPM fund market without guidance.

The premium pension system can be analysed from this division. The system provides two choices in the initial phase – to actively choose funds on the PPM fund market, or to consciously or

43

| Extended summary | SOU 2005:87 |

unconsciously refrain from making a choice with the consequence that premium pension money is instead invested in the Premiesparfonden.

As is evident, the fund market’s primary target group (target group 3) should be pension savers that feel they are knowledgeable and committed. Premiesparfonden should therefore presently fulfil the remaining investors’ needs (target groups 1 and 2), a considerable target group. We see that these investors probably have differrent needs depending on their level of knowledge and commitment in respect to managing their premium pension savings.

The committee is of the opinion that sufficient consideration has not been given to the need for

Draft for a future premium pension system

PPM fund market without guidance

| PPM fund | |||||||||||||||||||||

| market | Capital | ||||||||||||||||||||

| with | |||||||||||||||||||||

| guidance | market | ||||||||||||||||||||

Default alternative

| Informatíon | Guidance | Product |

44

| SOU 2005:87 | Extended summary |

The premium pension system’s default alternative

The premium pension system’s default alternative should have a generation fund profile, which means risk levels decline as the pension saver gets older. The entire collective general pension, including income and guarantee pension, should be considered when risk levels are determined in the default alternative. The default alternative should be an active choice option.

As a result of this proposal, Sjunde

The

PPM should in its traditional life insurance operations have the option to invest in funds on the market and in Sjunde

Limitations regarding Sjunde

Range of funds in the Premium Pension System

The range of funds in the system has increased heavily since the start. In the first round of fund choice in 2000, over 450 funds were registered in the system. At the close of September 2005, about 82 managers had registered 705 funds in the system. Each fund man-

45

| Extended summary | SOU 2005:87 |

ager had an average of 8.6 funds registered and the fund manager with the most funds had 36 funds registered.

The committee feels there should be a range of funds that provide a good return after investment fees and rebate. While it is in principle impossible to comment in advance on the funds’ returns, fund investment fees are set in advance. This means it is possible to influence the investment fees. A reasonable objective for PPM is therefore to keep the investment fees in the system at a low level.

One basis for the committee’s assessment has been that PPM will receive tools that mean the range of funds can be reduced to about

The committee is of the opinion that changes that need to be made should be made gradually. It is difficult to assess in advance the effect each measure will have on the range of funds. Naturally, it is even more difficult to judge the effects of a combination of different measures. The committee feels PPM should already now use the tools the authority has at its disposal to influence the range of funds.

According to the committee’s directives, the committee is also to consider the risk for systematically poor outcomes. The assignment does not refer to the risk for poor outcomes. Subsequently, the committee does not consider it a solution to exclude investment alternatives solely on the basis that they are expected to display a wide spread of returns over time. In addition, it is very possible that funds classified today as relatively

46

| SOU 2005:87 | Extended summary |

PPM’s tools to influence the range of funds

PPM has set a limit in which a fund manager may register maximum 25 funds with the authority. However, when several such fund managers make up the same management group, the group’s combined fund managers may register a combined maximum of 50 funds. The committee feels it should be considered if the current limits should be changed back to the number of funds that were permitted when the system was introduced (10 and 15 funds respectively). A family of generation funds should be counted as one fund.

In the capacity of investor PPM demands a rebate on the fund investment fee that pension savers pay. The discount is motivated by the fact that PPM carries a significant portion of such costs that otherwise would fall on the fund company, including distribution and customer service costs. The primary purpose of the discount is to ensure that pension savers receive a reasonable share of the benefits of economies of scale in investment management. Ac- cording to the committee, PPM should take steps to a greater extent transfer amounts to the pension savers which otherwise will become profits in the fund companies. The committee feels that PPM should continuously review the

According to the committee, PPM should use the option already available to extract a registration fee. Such a fee can be used to limit the influx of new funds.

New tools to influence the range of funds

PPM should be able to extract an annual feel for each fund registered with the authority.

It should be possible to introduce the option of setting a time limit within which a fund should achieve a certain market share in the system. Funds that cannot meet the time limit would subsequently be excluded from the selection.

47

| Extended summary | SOU 2005:87 |

Information to pension savers

PPM’s communication and information efforts during the first round of choice in 2000 must be considered very successful since one of the principal objectives was to achieve as many active choosers as possible. At the same time the result is not completely uncontroversial. It cannot be ignored that the campaign was very deliberate in its message to encourage savers to make a choice. In respect to providing

Despite the relatively extensive information activities conducted by the responsible authorities during the years after the first round of choice, conducted surveys indicate that many pension savers have not yet really understood what the

Alongside individual

48

| SOU 2005:87 | Extended summary |

Need for guidance

PPM should ensure that pension savers have access to guidance in form of

All pension savers should have access to

To facilitate pension savers’ management, their situation in making a choice should be made easier and they should also receive help in evaluating the choices they make. The committee feels that the issue of pension savers’ opportunities to evaluate their choices has not been sufficiently prioritised so far. Guidance in this aspect should contain reference objects that pension savers can use to evaluate their earlier choices with,

Questions about PPM’s annuity

In the long run, PPM should give pension savers the possibility to gradually switch from the

49

| Extended summary | SOU 2005:87 |

should instead provide and inform about alternatives that allow pension savers to even out the risk of their investments toward the close of their savings period. The committee proposes that it eventually be possible for pension savers to switch between the different insurance forms.

The committee does however feel that the government should appoint a special investigator to examine the conditions for dismantling PPM’s annuity activities. In practice this means there is a guarantee to premium pension savers that risks impacting on the government budget although the premium pension scheme is supposed to be autonomous. From this perspective the annuity can be described as an anomaly in the pension scheme. The investigator’s assignment should also include the forms for carrying out the actual dismantling of PPM’s annuity. In addition, a structure should be considered where such products are supplied by private

Until further notice, PPM’s annuity activities will remain intact. The committee therefore wants to emphasise the importance of keeping the guarantee to pension savers that the annuity entails at a low level. One possible option that the government should consider is to review the current product regulations for PPM’s annuity.

Administration of the

The problems that exist within the pension administration would to all extents be resolved by making an independent, separate authority responsible for pension administration. Without presenting a detailed proposal, the committee therefore suggests that a separate and independent pension authority be set up to handle pension administration.

50